- L-Plate Retiree

- Posts

- Fixed Income’s Strategic Buy Point – Why Bonds Deserve Another Look in 2025

Fixed Income’s Strategic Buy Point – Why Bonds Deserve Another Look in 2025

With yields near decade-highs and inflation risk still in play, fixed income offers opportunity — but only for investors who balance reward and caution

In partnership with

because retirement doesn’t come with a manual

Markets rallied as trade-hope and earnings momentum drove a welcome uptick

The quick scan: U.S. stocks closed higher on Monday, with broad gains driven by rising optimism around a potential U.S.–China trade framework and strong sentiment heading into tech earnings.

S&P 500: +1.23% to 6,875.16 – pushing to new record levels amid renewed risk appetite

Dow Jones: +0.71% to 47,544.59 – large-cap and industrial strength led the advance

NASDAQ: +1.86% to 23,637.46) – tech and semiconductors took the lead in the rally

What’s driving it: Markets lifted on growing confidence that the U.S. and China are nearing a trade deal, easing one of the largest overhangs on risk assets. At the same time, investors are warming up to the incoming wave of big-tech earnings and the prospect of a future rate cut from the Federal Reserve. With inflation data remaining benign and policy uncertainty gradually narrowing, risk-assets are regaining favour – at least for now.

Bottom line: For L-Plate Retirees this means: the market environment is improving – but it’s not time to abandon prudence. This is a good moment to check whether your portfolio’s allocation still aligns with your shared goals of stability and long-term growth. Keep your core holdings diversified, don’t chase the headlines, and consider building dry powder for any potential setbacks ahead.

How High-Net-Worth Families Invest Beyond the Balance Sheet

Every year, Long Angle surveys its private member community — entrepreneurs, executives, and investors with portfolios from $5M to $100M — to understand how they allocate their time, money, and trust.

The 2025 High-Net-Worth Professional Services Report reveals what today’s wealthy families value most, what disappoints them, and where satisfaction truly comes from.

From wealth management to wellness, from private schools to personal trainers — this study uncovers how the top 1% make choices that reflect their real priorities. You’ll see which services bring the greatest satisfaction, which feel merely transactional, and how spending patterns reveal what matters most to affluent households.

Benchmark your household’s service spending against peers with $5–25M portfolios.

Learn why emotional well-being often outranks financial optimization.

See which services families are most likely to change — and which they’ll never give up.

Understand generational differences shaping how the wealthy live, work, and parent.

See how your spending, satisfaction, and priorities compare to your peers. Download the report here.

Fixed Income’s Quiet Comeback

lock in yields with fixed income bonds

The scoop: After years of underwhelming returns, bonds are back in the spotlight – and this time, it’s not because they’re in trouble. A recent Business Times analysis notes that yields on quality fixed income have climbed to levels last seen before the Global Financial Crisis, creating what many analysts call a strategic buy point.

In simple terms, this means bonds are once again offering meaningful income. Where investors once earned next to nothing from government or investment-grade debt, they can now find yields in the 4–6 % range – without diving into high-risk territory. And because bond prices rise when rates eventually fall, the combination of income and potential capital appreciation makes this moment one of the most attractive fixed-income environments in over a decade.

For retirees and pre-retirees, this is a welcome reversal. With equity markets looking stretched and global growth cooling, bonds are reclaiming their classic role as both stabiliser and income generator. The article emphasised that “yield is destiny” – the higher the starting yield, the better the long-term return potential. In other words, today’s conditions may set the stage for stronger fixed-income performance through the rest of the decade.

But it’s not without risk. The piece cautioned that inflation remains a wild card – if it re-accelerates, central banks could keep rates higher for longer, capping bond-price gains. Longer-duration bonds, in particular, could suffer if yields rise further. There’s also the risk of credit deterioration in riskier segments of the market as slower growth squeezes weaker issuers. In short, the opportunity is real, but so is the need for discipline.

Actionable Takeaways for L-Plate Retirees

Revisit your allocations: If you’ve been underweight bonds, this could be a good time to rebuild exposure while yields remain appealing.

Stay quality-first: Prioritise investment-grade bonds and diversified bond funds over speculative issuers promising double-digit yields.

Mind the duration: Focus on short- to intermediate-term maturities to limit price sensitivity if rates rise again.

Lock in income, not just hope: Use the current high-yield window to secure steady income rather than chasing future capital gains.

Balance optimism with caution: Treat this as an entry point, not a guarantee – inflation, rate surprises, or credit shocks can still test even the safest bond portfolios.

Your turn:

How much of your portfolio provides steady, predictable income today?

If rates fell tomorrow, would you be glad you’d locked in these yields?

👉 Hit reply and share your thoughts – your answers could inspire fellow readers in future issues.

☕ If today’s read helped you see bonds as more than ballast, you can shout me a coffee on Ko-fi.

Resource:

Super Investors’ Club (SIC) – monthly membership subscription that aims to make learning about investing more hands-on and accessible to individuals on a mission to become financially free. Join here.

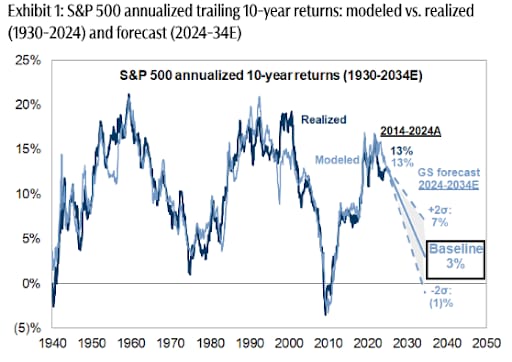

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

If these insights resonate with you, you’re in the right place. The L-Plate Retiree community is just beginning, and we’re figuring this out together-no pretence, no judgment, just honest conversation about navigating this next chapter.

Subscribe now to receive daily insights, practical tips, and the occasional laugh to help you thrive in retirement. We speak human here-no jargon without explanation, no assuming you’ve been investing since kindergarten.

And if today’s investing note hit the spot, you can buy us a coffee on Ko-fi ☕. Consider it your safest trade of the week-low risk, high return (in good vibes).

Because retirement doesn’t come with a manual… but now it does come with this newsletter.

The L-Plate Retiree Team

(Disclaimer: While we love a good laugh, the information in this newsletter is for general informational and entertainment purposes only, and does not constitute financial, health, or any other professional advice. Always consult with a qualified professional before making any decisions about your retirement, finances, or health.)

Reply