- L-Plate Retiree

- Posts

- The Silent Threat to Retirement Nest Eggs That Most People Never See Coming

The Silent Threat to Retirement Nest Eggs That Most People Never See Coming

Why playing it “too safe” with your investments can quietly shrink your future income

In partnership with

because retirement doesn’t come with a manual

Balance is the key to life, and it turns out it is just as essential in our retirement portfolios as it is anywhere else. Today’s article is a good reminder that staying too safe can be its own kind of risk. I also believe there is value in learning skills that help you generate income even in retirement. Trading is one of them. Done right, it does not need to be high risk. And like most things worth knowing, it can be taught. If you are curious, check out Iris’ masterclass below.

CS

Stocks jump as rate-cut hopes reignite in thin holiday week trading

The quick scan: Markets rebounded strongly, showing that investors are willing to take a breather after recent volatility and roll some risk back in as chances of a Fed rate cut next month climb. The tone is one of cautious optimism rather than full confidence.

S&P 500: +1.55% to 6,705.12 – rallied as broad participation returned

Dow Jones: +0.44% to 46,448.27 – blue-chips benefited from easing yields

NASDAQ: +2.69% to 22,872.01 – tech and growth stocks led the charge

What’s driving it: Two main factors are behind the bounce. First, comments from senior Fed officials suggesting a rate cut is still on the table gave a fresh tailwind to markets. That reignited some of the risk appetite that had faded. Second, after a week of sharp losses and market jitters, many traders appear to be seeing an opportunity to buy on weakness rather than waiting on the sidelines. While liquidity is lighter this week (thanks to the upcoming holiday), the message is still meaningful: when policy expectations shift, markets respond quickly. That said, lurking risks (inflation, valuations, global growth) remain, so this rally should be seen as a pivot point – not a moment of clarity.

Bottom line: For L-Plate Retirees this is a useful reminder that market sentiment can flip before fundamentals fully catch up. It doesn’t mean dive in headfirst, but it does mean check whether your portfolio is positioned to benefit from the next leg of the journey – rather than watching from the sidelines.

Turn AI Into Your Income Stream

The AI economy is booming, and smart entrepreneurs are already profiting. Subscribe to Mindstream and get instant access to 200+ proven strategies to monetize AI tools like ChatGPT, Midjourney, and more. From content creation to automation services, discover actionable ways to build your AI-powered income. No coding required, just practical strategies that work.

The Risk Hiding in Your Retirement Plan

savings is not an investment

The scoop: Today’s article highlights a danger many retirees overlook because it feels so sensible at first: becoming too conservative with your investments. As we age, it’s natural to shift toward safety. Cash feels comfortable. Term deposits feel predictable. Bonds feel reassuring. After all, who wants wild swings when you’re trying to fund the next 20 or 30 years of life?

But the Allan Hall team makes one thing uncomfortably clear. When interest rates sit low for extended periods, when inflation keeps nibbling at purchasing power and when people are living longer than ever, excessive caution becomes its own kind of risk.

It’s the quiet kind. The kind that doesn’t show up in scary headlines. The kind that does not trigger phone calls from your adviser. The kind that doesn’t happen in one big moment.

This erosion happens slowly. Month by month. Year by year.

A little less growth here.

A little less income there.

Higher prices on groceries and utilities.

Medical costs creeping upward.

Life expectancy stretching further.

And because it is gradual rather than dramatic, many retirees don’t recognise the threat until much later when withdrawals start feeling heavier and savings no longer climb the way they used to.

The article puts the spotlight on an uncomfortable truth: the very strategies meant to keep your nest egg safe can unintentionally shrink it over time.

This does not mean retirees should leap into high-risk assets. Rather, it’s about understanding that long-term growth is still essential well into retirement. Life is longer. Inflation is persistent. Cash rates are unpredictable. And money left sitting too quietly can fall behind the life you want to live.

The antidote? Purposeful diversification, steady exposure to growth assets and a clear plan that balances safety with sustainability. It’s less about being fearless, more about being realistic with the number of years ahead of you and the lifestyle you hope to maintain.

Actionable takeaways for L-Plate Retirees:

Check your risk balance. If you have shifted too heavily into cash or low-return assets, consider whether your portfolio can still grow enough to serve a long retirement.

Plan for a longer road. Build your retirement strategy with the expectation that you will live longer than previous generations. Growth becomes more important, not less.

Watch inflation’s quiet bite. Even mild inflation can erode a static portfolio. Make sure part of your nest egg has the potential to outpace rising costs.

Use diversification as protection. A mix of income, defensive and growth assets spreads risk more effectively than relying on one type of investment.

Seek sustainability over comfort. The goal is not zero volatility, but a portfolio that supports your lifestyle over decades. Sometimes a little discomfort today prevents a bigger issue later.

Your Turn:

Which part of your portfolio might be working too quietly to support your future needs?

Have you ever shifted to safety only to realise later that growth still mattered?

If you could strengthen one part of your investment plan this month, what would you choose?

👉 Hit reply and share your thoughts – your answers could inspire fellow readers in future issues.

If today’s issue helped you think differently about protecting your nest egg, you can shout me a coffee on Ko-fi. It keeps this little community fuelled and thoughtful.

Resources:

Super Investors’ Club (SIC) – monthly membership subscription that aims to make learning about investing more hands-on and accessible to individuals on a mission to become financially free. Join here.

* * * * *

If you’ve ever wished someone would just explain the markets without the noise, this might be worth a look.

I watched this session myself and found it surprisingly clear – no hype, no pressure, just practical ways to approach the market with a calmer, more methodical mindset.

If you’re curious, you can take a peek here:

👉 Explore the Stock Sniper webinar

* * * * *

Options can be a useful tool if you understand how to manage risk – especially in retirement, where protecting capital matters more than chasing big wins.

This workshop focuses on exactly that: the “slow, steady, sensible” side of options.

If you’d like to learn the basics without feeling overwhelmed, here’s the link:

👉 Check out the Options Workshop

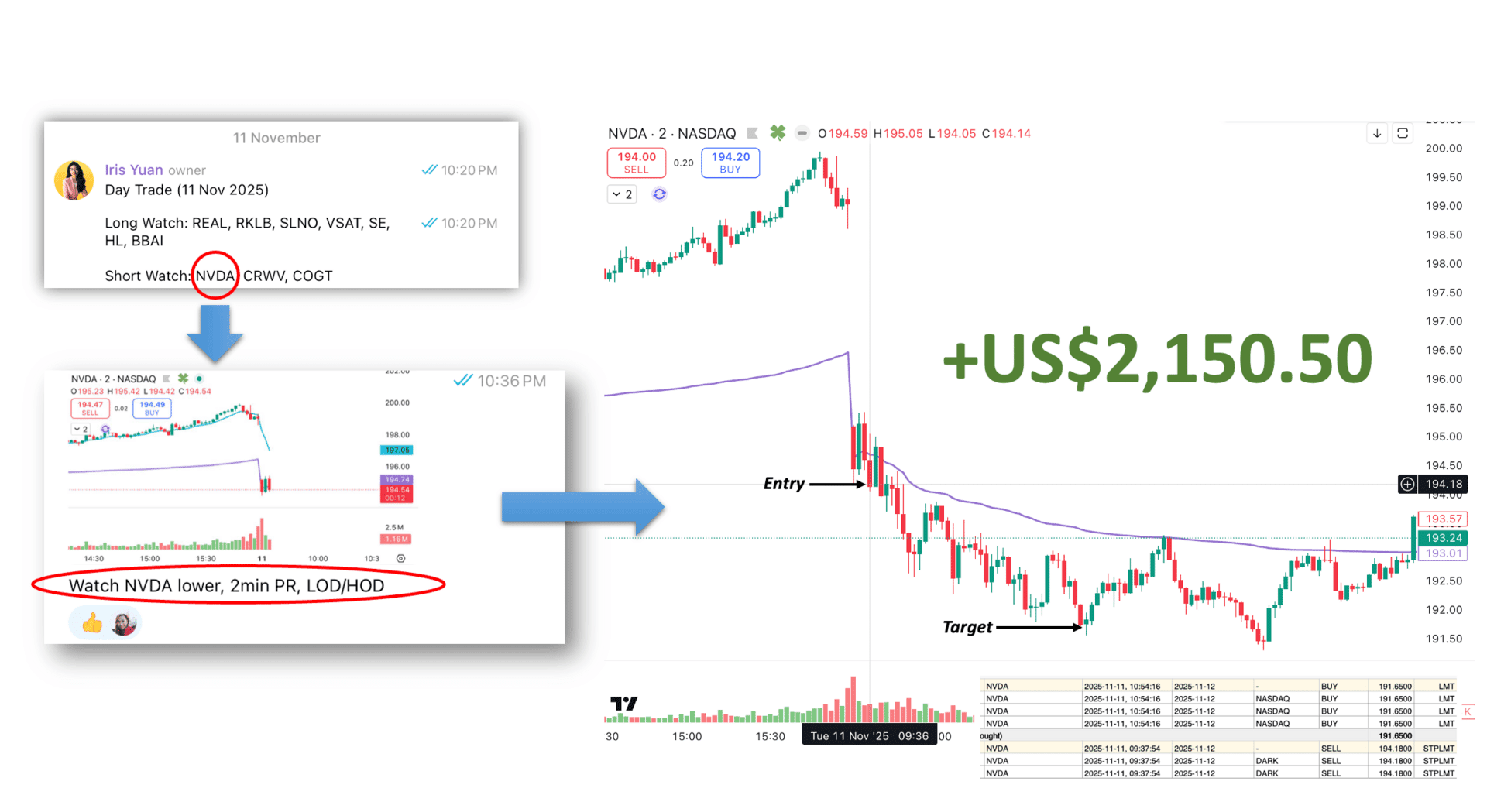

How Iris, the Stock Sniper, made $2,150 in 7 minutes

Two weeks ago, Iris executed a pre-planned NVDA trade that hit USD 2,150.50 in profit.

The trade took 80 minutes to reach its target profit but she only spent 7 minutes actively managing it.

How?!

Everything was planned – entry, exit, target, and risk.

She simply clicked once and let the system do the work.

This is what trading looks like when you stop grinding and start systemizing.

Most traders think trading is:

Staring at monitors all day

Chasing every price move

Working harder to make more

Iris proved the opposite. She trades one hour a day and consistently wins. Her core rules are:

Let your Capital work for you: trades may take time to hit – but they should not take your time

Recognise setups, don’t predict: when the signs align, execute

Plan, trust, relax: the system works – you don’t have to

Her results speak for themselves, bull or bear market:

2022: +$108,176 profit (this, when market was down 22%)

2023: +$109,435 profit

2024: +$112,718 profit

Now, Iris is opening up her 1-hour-a-day trading system in a free 2-hour masterclass where you’ll learn:

Scan → Shortlist → Execute →Log off in 60 minutes

Build a watchlist that does the heavy lifting

Clean-chart rules for faster, clearer decisions

Risk management that keeps losers small and winners running

How to trade even if you are away from your screen

This isn’t theory. It’s the same system that made $2,150 in a day last week, and 6-figure profits year after year.

If you’re ready to stop trading your time for money and take control of your schedule, income and peace of mind, sign up for the Masterclass now!

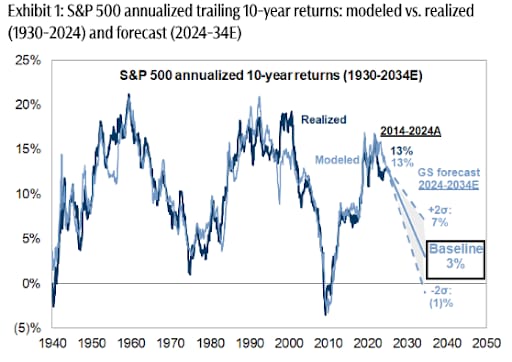

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

If these insights resonate with you, you’re in the right place. The L-Plate Retiree community is just beginning, and we’re figuring this out together-no pretence, no judgment, just honest conversation about navigating this next chapter.

Subscribe now to receive daily insights, practical tips, and the occasional laugh to help you thrive in retirement. We speak human here-no jargon without explanation, no assuming you’ve been investing since kindergarten.

And if today’s investing note hit the spot, you can buy us a coffee on Ko-fi ☕. Consider it your safest trade of the week-low risk, high return (in good vibes).

Because retirement doesn’t come with a manual… but now it does come with this newsletter.

The L-Plate Retiree Team

(Disclaimer: While we love a good laugh, the information in this newsletter is for general informational and entertainment purposes only, and does not constitute financial, health, or any other professional advice. Always consult with a qualified professional before making any decisions about your retirement, finances, or health.)

Reply