- L-Plate Retiree

- Posts

- Your Past Isn't Your Prison: Why Context Matters More Than Regret in Retirement

Your Past Isn't Your Prison: Why Context Matters More Than Regret in Retirement

The financial mistakes, fitness failures, and wrong turns don't cage you – they explain you. Here's how changing the lens changes everything.

In partnership with

because retirement doesn’t come with a manual

the famous/ notorious alcatraz prison in the US of A

There's a phrase I heard recently from a pastor that's been quietly following me around all week.

Your past is not your prison.

It's tempting to treat the past like a locked cell – something we either try to escape from, pretend never happened, or quietly resent every time it rattles its keys. I've certainly done all three at various points, sometimes on the same Tuesday.

But maybe that's the wrong metaphor altogether.

What if the past isn't a prison... but context?

Because like it or not, we all have a story. Not the Instagram version. The real one.

The detours. The decisions we'd love to Ctrl+Z. The habits that stuck longer than planned. The investments that didn't quite work out. The fitness routines that started enthusiastically in January and ended mysteriously around Valentine's Day when chocolate became more appealing than burpees.

When we don't like our story, the instinct is to edit it. Delete a chapter here, rewrite a paragraph there, maybe add a redemption arc that sounds better at dinner parties.

But here's the thing – the story already happened.

What can change is how we interpret it.

There's a subtle but powerful difference between seeing your past only as a list of mistakes versus recognizing it as a series of lessons that shaped how you think, act, and decide today.

Same events. Different lens.

If you replay your financial history purely as "I should have known better," it becomes a source of guilt. Every market crash you didn't predict, every stock you bought too high, every dollar you spent on something that seemed important at the time but now feels ridiculous.

But if you see it as "this taught me how risk actually feels," it becomes experience. The kind you can't get from reading books or watching YouTube tutorials. The visceral, stomach-dropping understanding that comes only from living through the consequences of your choices.

Same story. Different interpretation.

If you frame your health journey as "I let myself go," it becomes shame. All those years you meant to exercise but didn't. The weight that crept on so gradually you barely noticed until suddenly your clothes didn't fit and your knees started complaining about stairs.

But if you frame it as "this showed me what happens when routines disappear," it becomes information. Data you can actually use going forward instead of just evidence for why you're a failure.

The danger isn't the past itself – it's interpreting it with the wrong narrative.

When we remember without meaning, all we retrieve are emotions. Regret, embarrassment, frustration. And those emotions have a funny way of trying to drive the future, like a backseat driver who won't shut up about that wrong turn you took in 2008.

But the past doesn't get to vote anymore.

It can inform the future – yes. It can shape priorities – absolutely. It can even explain why certain financial decisions make you nervous or why you're particularly motivated about health now.

But it doesn't get to decide what happens next. That's still your call.

This matters enormously as we move through this phase of life, because it's easy to think:

"It's too late to get fitter."

"I've already missed the best investing years."

"This is just how my body works now."

"I've always been bad with money."

Those aren't facts. They're interpretations. Stories we tell ourselves about ourselves, usually without stopping to question whether they're actually true or just comfortable narratives we've repeated so many times they've calcified into identity.

The future is still very much in your hands.

What you eat this week still matters. How you move your body still matters. How you save, invest, and manage risk still matters.

Not because the past disappears – it doesn't. The market crash you lived through still happened. The years of minimal exercise still count. The money choices that didn't work out are still part of your story.

But they become context instead of a cage.

Maybe that's the quiet invitation of retirement planning, health, and money at this stage of life – not to erase the story, but to reread it with a wiser lens.

To say:

"This is how I got here. These are the things that scared me, challenged me, shaped me. Some of them are still hanging around, and I'm still figuring out how to deal with them.

This is what I've learned – often the hard way, sometimes the expensive way, occasionally the painful way.

And this is what I choose to do next."

Because the past explains you. It provides context for why you make the decisions you make, why certain things trigger anxiety while others feel manageable, why you're cautious in some areas and bold in others.

But it doesn't imprison you.

The investment mistakes don't mean you can't invest wisely now. The fitness failures don't mean movement is pointless. The financial detours don't determine your destination – they just explain part of the route.

And the next chapter? Still unwritten.

You're holding the pen.

Your Turn:

What story about your past have you been treating as a prison when it might actually just be context?

If you rewrote your financial or health history as "this is what I learned" instead of "this is where I failed," what would change?

What's one choice you could make this week that proves the past explains you but doesn't control you?

👉 Hit reply and share your thoughts – I’d love to hear what’s resonating with you.

☕ Your support keeps L-Plate Retiree exploring the messy, honest territory between who we were and who we're becoming. If these weekend reflections resonate with your own experience of rewriting old stories, you can shout us a coffee on Ko-fi.

The New Year Ritual That Sets the Tone for Energy and Glow ✨

January calls for rituals that actually make you feel amazing—and Pique’s Sun Goddess Matcha is mine. It delivers clean, focused energy with zero jitters, supports glowing skin and gentle detox, and feels deeply grounding. Smooth, ceremonial-grade, and crave-worthy, it’s the easiest way to start your day clear, energized, and glowing from the inside out.

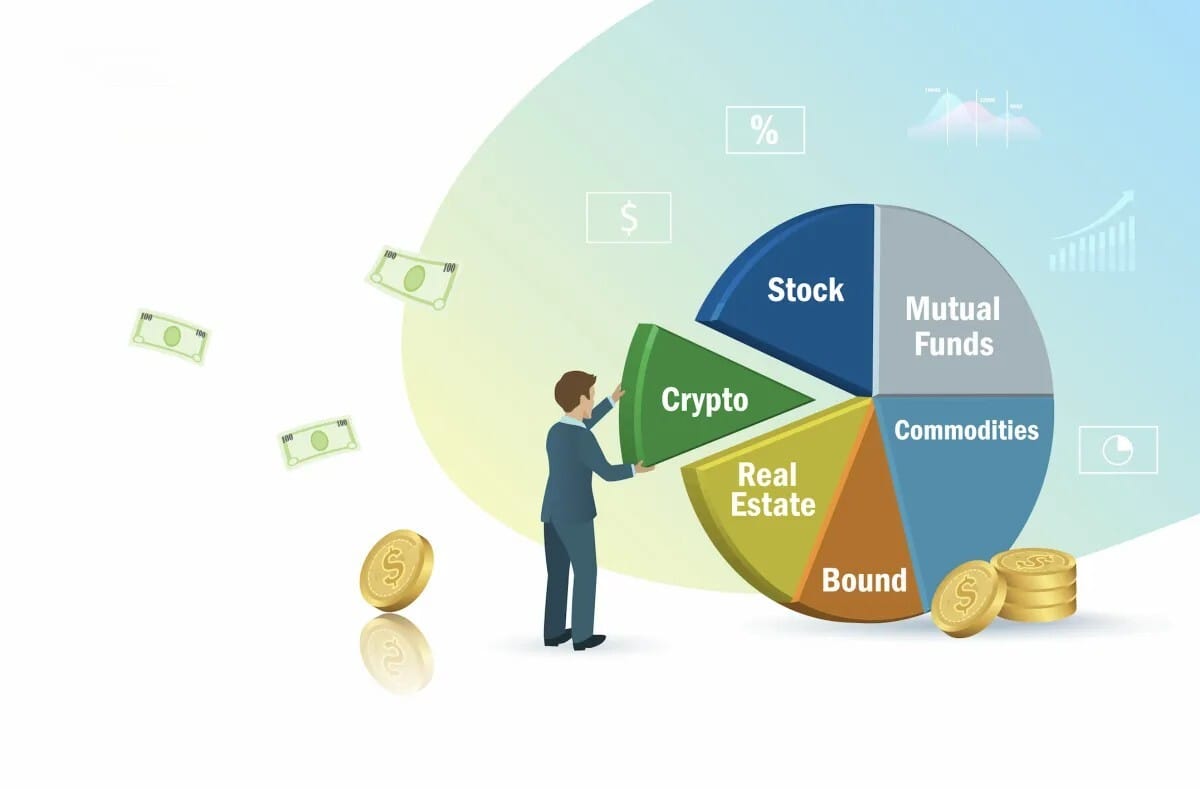

The Science of Portfolio Building

portfolio building is all about diversification

We've set our blueprint with Asset Allocation. Now, let's look at the science behind how we choose and combine those assets. This is Portfolio Construction, and it's all about getting the most return for the least amount of risk – the ultimate goal of Risk and Return Fundamentals.

The classic approach is Modern Portfolio Theory (MPT). The big idea here is diversification. MPT says that by combining assets that don't move perfectly in sync (i.e., they are not perfectly correlated), you can reduce the overall portfolio volatility without sacrificing return. Think of it like this: when your stocks are having a bad day, your bonds might be having a good day, smoothing out the ride. MPT aims to find the "efficient frontier" – the best possible return for every level of risk.

But MPT has a slightly more modern cousin: Post-Modern Portfolio Theory (PMPT). Some investors argue that they only care about downside risk – the risk of losing money – not volatility on the upside. PMPT uses different metrics, like the Sortino Ratio, which only penalizes a portfolio for returns that fall below a certain target. This is often more psychologically appealing for L-Plate Retirees who are primarily concerned with capital preservation.

Then there's the concept of Risk Parity. This is a different way of thinking about diversification. Instead of allocating capital equally (e.g., 50% stocks, 50% bonds), you allocate capital so that each asset class contributes equally to the total portfolio risk. Since bonds are generally less volatile than stocks, a risk parity portfolio will typically hold a much higher percentage of bonds, which are then sometimes leveraged to achieve the desired return. It's a more sophisticated approach, but the core idea is a deep commitment to diversification.

For most L-Plate Retirees, the core takeaway is the power of MPT's diversification principle. You don't need to be a math whiz to benefit from it. Simply combining different asset classes (stocks, bonds, real estate, cash) is the most effective way to build a robust portfolio.

L-Plate Takeaways

MPT's Core Idea is Diversification: Combine assets that don't move in sync to reduce overall portfolio risk without sacrificing return.

PMPT Focuses on Downside Risk: This theory is more concerned with avoiding losses than with overall volatility, which can be appealing for conservative investors.

Risk Parity is Risk-Based Allocation: Instead of allocating capital equally, you allocate based on how much risk each asset contributes.

Keep it Simple: For L-Plate Retirees, implementing MPT is as simple as using low-cost, diversified funds across different asset classes.

The Efficient Frontier: The goal of portfolio construction is to find the best possible return for the level of risk you are willing to take.

Support Your New Years Resolutions with CBD

Setting a New Years resolution is a lot easier than keeping it. But CBDistillery’s expertly-formulated CBD products make sticking with your resolutions easier. Save 25% on CBD to ease pain after workouts, stress less, sleep better or unwind alcohol-free with code HNY25 and keep your resolutions on track.

The L-Plate Retiree community is just beginning, and we’re figuring this out together – no pretense, no judgment, just honest conversation about navigating this next chapter.

Subscribe now, or share it with a friend, to get weekly insights, practical tips, and the occasional laugh to help you prepare for or thrive in retirement. Unlike other newsletters that assume you already know everything, we keep it simple and human.

And if today’s musings brightened your day, you can toss a coffee into our Ko-fi tip jar ☕. Think of it like leaving a tip for your favourite busker – only this busker writes about retirement.

Because retirement doesn’t come with a manual… but now it does come with this newsletter.

The L-Plate Retiree Team

(Disclaimer: While we love a good laugh, the information in this newsletter is for general informational and entertainment purposes only, and does not constitute financial, health, or any other professional advice. Always consult with a qualified professional before making any decisions about your retirement, finances, or health.)

Reply